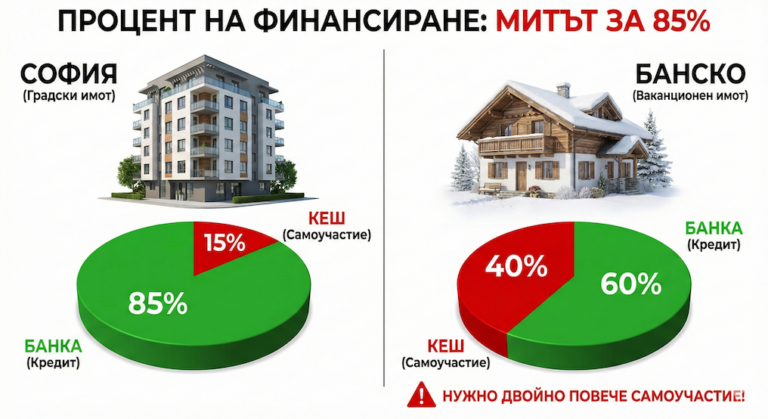

The credit officer looks at the location "Bansko" and in an even tone reports: „"Unfortunately, for this area and property type, the maximum financing percentage (LTV) is 60%. You must provide the remaining 40% plus expenses yourself."“

Warning: Financial shock!

This is the moment when many deals fall apart right from the start. The buyer has prepared 10,000 euros, but it turns out that he needs 25,000 euros. In this article, we will explain why banks treat Bansko as a „higher risk“ market and why they require you to double or triple the deductible in 2026.

1. Financing Percentage (LTV): Urban vs. Vacation Property

The banking term you need to remember is LTV (Loan-to-Value) – the ratio between the loan amount and the market value of the property. Here's what the gross difference looks like in numbers:

-

Main residence (Big city)

The bank finances up to 85% – 90%.

Example: Property for 60,000 EUR. The bank gives 51,000 EUR. You pay 9,000 EUR cache.

-

Holiday property (Bansko)

The bank finances between 50% and 70% (at best).

Example: Property for 60,000 EUR. The bank gives 36,000 EUR. You pay 24,000 EUR cash!

2. Why is the bank making me pay more? (The 3 reasons)

Don't take this personally. The bank is not questioning your income, but the liquidity of the collateral. It is simply managing its risk. Here's what specifically worries bankers in Bansko:

Reason A: The Psychology of the „Second Home“

Banking statistics are merciless: When a household falls into a severe financial crisis, it stops servicing its obligations in strict order. First, credit card payments stop, then the car lease, and immediately after that, the mortgage on the vacation property. The down payment on the main residence (where the family lives) is paid to the last, at any cost.

For the bank, a property in Bansko is a "luxury" that you would most easily give up in the event of a problem. That's why they want you to take on a larger share of the risk ("skin in the game") right from the start through a high deductible.

Reason B: Lower and seasonal liquidity

„Liquidity“ is the speed at which an asset can be converted into money. If the bank has to take your property and sell it at auction, in Sofia this can happen in 1-2 months. In Bansko, despite the year-round flow of tourists and nomads, the market is still slower and highly dependent on the season. The bank is afraid that if it has to urgently sell your apartment in May or November, it will have to lower the price drastically. So they insure themselves by giving you less money.

Reason B: The specifics of the complexes and fees

Some banks maintain an internal „blacklist“ of complexes in Bansko. If the property is in a building with a bad reputation, unclear ownership, a huge maintenance fee (which makes the property difficult to sell) or structural problems, the financing rate can drop to 40-50%, regardless of how solvent you are as a client.

Expert advice: How to "cheat" the system?

If you don't have the necessary large deductible (e.g. 25,000 euros), but you have good income, there is a completely legal and working option: Additional collateral. Offer the bank to mortgage a property in a large regional city (your parents' or another property of yours without a mortgage). When the collateral is an apartment in Sofia, Plovdiv or Varna, the bank can finance you on 100% for the purchase in Bansko, with a lower interest rate, typical of a housing loan.

3. Reality: Exactly how much money do you need in 2026?

Let's be realistic and talk in concrete numbers. If you're planning a purchase in Bansko this year, here's how much money you should have available "in your pocket" before you even step foot in the bank:

| Property Type / Status | Expected financing (Bank) | Copayment required (Your money) |

|---|---|---|

| Apartment in a residential building (No maintenance fee, Act 16) |

up to 70% – 75% | 25% – 30% |

| Apartment in a hotel complex (High fee, Atelier status) |

50% – 60% | 40% – 50% |

| Panel block (Old building in the city) |

50% – 60% | 40% – 50% |

Don't forget the hidden costs!

In addition to this high deductible, you need about 5% to 8% from the cash price to cover notary fees, local tax (3% for Bansko), brokerage commission and registration fees. The bank never finances these costs!

Conclusion

The myth of "easy and cheap financing" in Bansko often breaks down at the wall of the requirement for high co-payment. If you are used to the liberal conditions in Sofia, here the rules of the game are different. To buy a property under Todorka in 2026, you must be financially disciplined and prepared with more serious equity.

However, this also has its good side - a higher deductible means a smaller loan and, accordingly, a smaller monthly payment. This makes it much more realistic to cover the mortgage through rental income, which we talked about in our previous analyses.

Looking for the bank with the highest financing rate?

Not all banks are the same. We know which lenders currently have an "appetite" for Bansko properties and offer up to 75-80% financing on preferential terms.